Capital Gains Tax in the United States

If you sold your land or stocks for more than you paid, you’ve made a profit and that profit is called a capital gain. The IRS usually wants a share of that money and that is capital gains tax. It’s a tax on the profit you make from selling something valuable. Whether it’s real estate, investments, or even cryptocurrency, knowing how capital gains tax works can help you avoid surprises, lower your tax bill, and keep more of your money.

What Is Capital Gains Tax?

Capital gains tax is a tax you pay when you make money by selling something valuable for more than what you paid for it. That something could be things like a house, land, stocks, crypto, gold, or even a rare painting. Imagine you bought some shares for $5,000 and later sold them for $7,000. That extra $2,000 is your profit. And since it’s income you made, the government wants a piece of it. You don’t pay this tax when you buy the item, only when you sell it and make a profit. So if you’re planning to sell something valuable.

Short-Term vs Long-Term Capital Gains

Capital gains tax depends on how long you hold onto something before selling it really matters. The IRS splits capital gains into two types: short-term and long-term, and each one is taxed differently.

Short-Term Capital Gains

If you sell something you've owned for a year or less like a stock, land, or even crypto any profit you make is considered a short-term capital gain. These gains are taxed just like your regular income. So if you’re in the 24% income bracket, your gain gets taxed at 24%, just like your paycheck would.

Long-Term Capital Gains

Now, if you hold onto that same asset for more than one year before selling, the rules change in your favor. These are called long-term capital gains, and they’re taxed at lower rates either 0%, 15%, or 20%, depending on how much you earn in total. This is why many smart investors prefer to wait. Holding your investment for at least a year could save you a decent amount in taxes when you finally decide to sell. It’s like a reward for being patient.

What Kinds of Things Are Subject to Capital Gains Tax?

Capital gains tax doesn’t just apply to big investments like stocks or houses. It can show up in lots of everyday things. If you make a profit from selling stocks, bonds, real estate (like a second home), cryptocurrency, or even collectibles like baseball cards or rare coins, you could owe tax on that gain. Believe it or not, even selling sneakers or comic books online for a profit can count. If you bought something and sold it for more than you paid, that extra money is usually seen as a capital gain and yes, it can be taxed.

Capital Gains Tax Rates for 2025

long-term capital gains tax rates based on your income:

|

Filing Status |

0% Rate |

15% Rate |

20% Rate |

|

Single |

Up to $47,025 |

$47,026–$518,900 |

Over $518,900 |

|

Married Filing Jointly |

Up to $94,050 |

$94,051–$583,750 |

Over $583,750 |

|

Head of Household |

Up to $63,000 |

$63,001–$551,350 |

Over $551,350 |

Keep in mind, if you’re selling a home, there are some special rules we’ll get into below.

Do You Always Have to Pay Capital Gains Tax?

Not every profit you make gets hit with capital gains tax there are a few situations where you can skip it or lower the amount you owe. Knowing these can save you thousands, especially if you're planning a big sale.

Selling Your Primary Home

If the home you’re selling is your main residence and you’ve lived in it for at least 2 out of the last 5 years, you might not owe any capital gains tax at all. You can exclude up to $250,000 of profit if you're single or up to $500,000 if you’re married and file jointly. So, if you bought a house for $200,000 and sold it for $700,000, a married couple could keep that $500,000 gain tax-free. That's a big win for homeowners.

Low Income = 0% Tax

If your income is on the lower side, you might qualify for the 0% long-term capital gains tax rate. For 2025, if you're single and your taxable income is up to $47,025, or married and under $94,050 combined, you could sell investments you’ve held for over a year and pay nothing in capital gains tax.

Retirement Accounts

Your 401(k), IRA, or other retirement accounts. Any profits made inside these accounts aren’t subject to capital gains tax while the investments grow. Instead, you pay regular income tax when you take the money out usually after retirement. So if you bought shares inside your IRA and they doubled in value, you won’t owe anything until you withdraw the funds later. It’s one reason why these accounts are powerful tools for long-term investing.

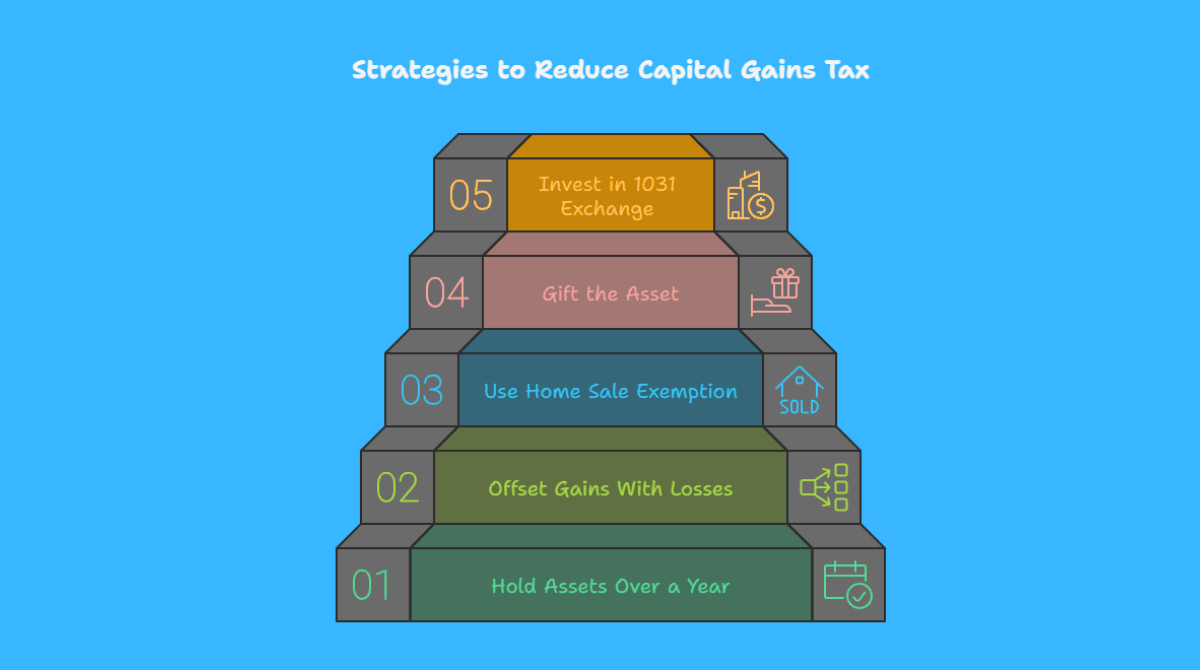

How to Reduce or Avoid Capital Gains Tax

There are smart, legal ways to reduce capital gains tax or even avoid it in some cases. With the right planning, you can keep more of your money where it belongs in your pocket.

Hold Assets for Over a Year

If you hold your asset for more than one year, you qualify for the lower long-term capital gains tax rate. Instead of paying up to 37% for short-term gains, you might pay just 15% or even 0%, depending on your income. So, if you’re thinking of selling at 11 months, it may be worth waiting one more month to save thousands.

Offset Gains With Losses

If you gained $2,000 on one stock but lost $1,500 on another. You can subtract the loss from your gain and only be taxed on the $500 profit. If your losses are more than your gains, you can deduct up to $3,000 from your regular income and carry the rest forward into future years.

Use the Home Sale Exemption

If you’re selling your main home, the IRS gives you a major break. As long as you’ve lived in the house for 2 of the last 5 years, you can avoid capital gains tax on up to $250,000 in profit if you’re single or up to $500,000 if married filing jointly. So, if you bought your home for $300,000 and sell it for $800,000, a married couple can keep that entire $500,000 profit tax-free. This is one of the biggest tax breaks most people ever get, and it’s worth taking full advantage of.

Gift the Asset

Instead of selling your stocks or property yourself, you can gift them to a family member in a lower income bracket like a student or a retired parent. Let’s say your stock has gone up by $10,000. If you’re in the 35% tax bracket, you’d owe $3,500 in capital gains tax. But if you gift it to your child who’s in the 0% bracket, and they sell it, there may be no tax at all. Just make sure the gift stays within the IRS’s annual limit of $18,000 per person in 2025 to avoid triggering gift taxes.

Invest in a 1031 Exchange (Real Estate)

If you’re selling investment property, a 1031 exchange can help you delay the capital gains tax. For example, if you sell a rental property and make a $100,000 profit, you can reinvest that money into another similar property and avoid paying tax right away. You have to follow strict rules like identifying the new property within 45 days and closing the deal within 180 days.

What If I Don’t Report Capital Gains?

The IRS already knows about most of your capital gains, especially from things like stocks or crypto. Your broker or exchange usually sends them a Form 1099-B, so if you skip reporting it on your tax return, you’re likely to get a letter later asking why. You could face interest charges or even penalties.

Capital Gains Tax and Real Estate

If you bought a house for $180,000 and sold it later for $280,000 you made a $100,000 profit. If it was your main home and you lived there for at least 2 of the last 5 years, you likely won’t pay capital gains tax on that. But if it was a rental or second home, that $100,000 could be fully taxable. You might also owe extra if you claimed depreciation while renting it out. So, whether or not you pay tax depends on how you used the property not just the sale price.

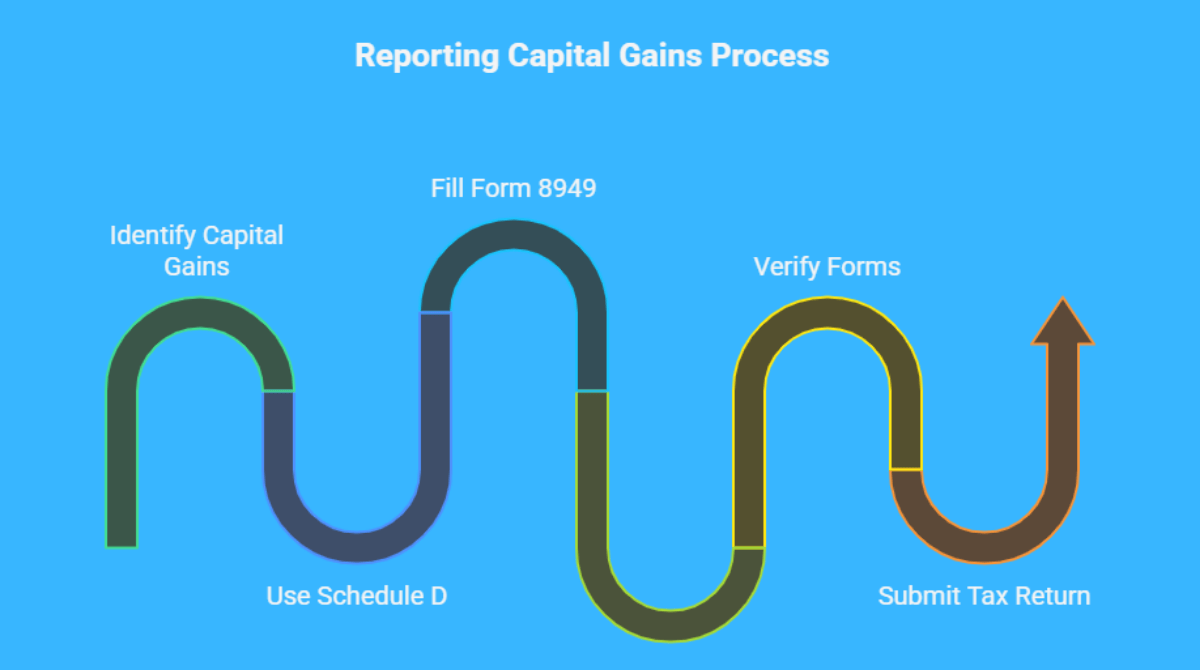

What Forms Do I Need to Report Capital Gains?

When you sell something for a profit like stocks, crypto, or property you’ll need to report it during tax season. Here are the key forms involved:

-

You’ll use Schedule D (Form 1040) to summarize all your capital gains and losses from the year in one place.

-

Details of each sale, like dates and amounts, go on Form 8949, where you show what you sold, how much you paid, and what you made.

-

If you sold through a broker or exchange, expect a 1099-B form from them it lists each transaction and helps you fill in the other forms correctly.

Tax software can usually handle all this automatically, but it helps to know what each form does in case something looks off or you need to explain it later.

Are there Capital Gains on Crypto?

Capital gains tax applies when you sell or trade cryptocurrency for a profit. So if you bought Bitcoin at $10,000 and sold it later for $18,000, that $8,000 gain is taxable. And it’s not just when you cash out to dollars even swapping one crypto for another, like trading Ethereum for Solana, triggers a taxable event. The IRS sees it the same way as selling stock.

Need help with Capital Gains Tax?

If you're selling property, cashing out investments, you don’t have to figure it all out by yourself. We’ve been helping people with capital gains tax for over 20 years whether it’s real estate, stocks, or crypto and we know how to build a smart strategy that helps you keep more of your money. Just reach out for a free consultation and we’ll walk you through everything, step by step.

Conclusion

Understanding capital gains tax really helps. With a bit of strategy like timing your sale right, using your losses wisely, or simply getting the right advice you can cut down what you owe and keep more in your hands. It’s not about avoiding tax; it’s about being smart with your money.

FAQs

1. Do I have to pay capital gains tax if I reinvest the money?

Yes. Just because you use the profit to buy something else doesn’t mean the IRS gives you a pass. Unless it’s in a retirement account or a 1031 exchange for real estate, you still owe tax on the gain.

2. I sold something at a loss do I still report it?

Definitely. Losses can actually help. You can use them to cancel out gains and even take up to $3,000 off your regular income. And if your loss is bigger you can roll the rest into next year.

3. Is inherited property taxed the same way?

Not really. If you sell it soon after inheriting, you probably won’t owe much tax. The value resets to what it was when the person passed away, not what they paid years ago.

4. I got paid in crypto. Is that a capital gain?

Getting paid in crypto is treated like income first. But if that crypto goes up in value and you sell it later, then you pay capital gains tax on the profit.

5. What if I sell a house I own with someone else?

You each report your share of the profit. So if you sell a house and make $40,000 in gains, and you own half, you’d each report $20,000.

6. Can capital gains affect my other taxes?

Yes. Even if the rate is lower, big gains can push up things like Medicare costs or reduce your tax credits. It adds to your overall income, and that can quietly raise your bill.

Follow SKFinancial on Facebook / Twitter / Linkedin / Youtube for updates.